Torque is cheap

Also: activism, passivism, private credit, philanthropy, supercars, Meta biscuits, and who's going to win the World Cup

In the early months of 2000, during your correspondent's first tour of duty, a London-listed capital goods maker invited the press to attend the midday launch of its internet strategy. What exactly this company did isn't important now, and wasn't then. The invite said "internet", so the share price doubled. Newsrooms dispatched cub reporters to the firm's wood-panelled office, where we heard the chairman announce that its next annual report would be made available "in electronic document format".

Everything’s more sophisticated these days. Post the dotcom bubble, a company can’t just drop buzzwords like “blockchain”, “metaverse” and “tokenisation” into a presentation and watch its shares motor. The specific words and phrases it needs to use are “agentic”, “humanoid” and “data centre”.

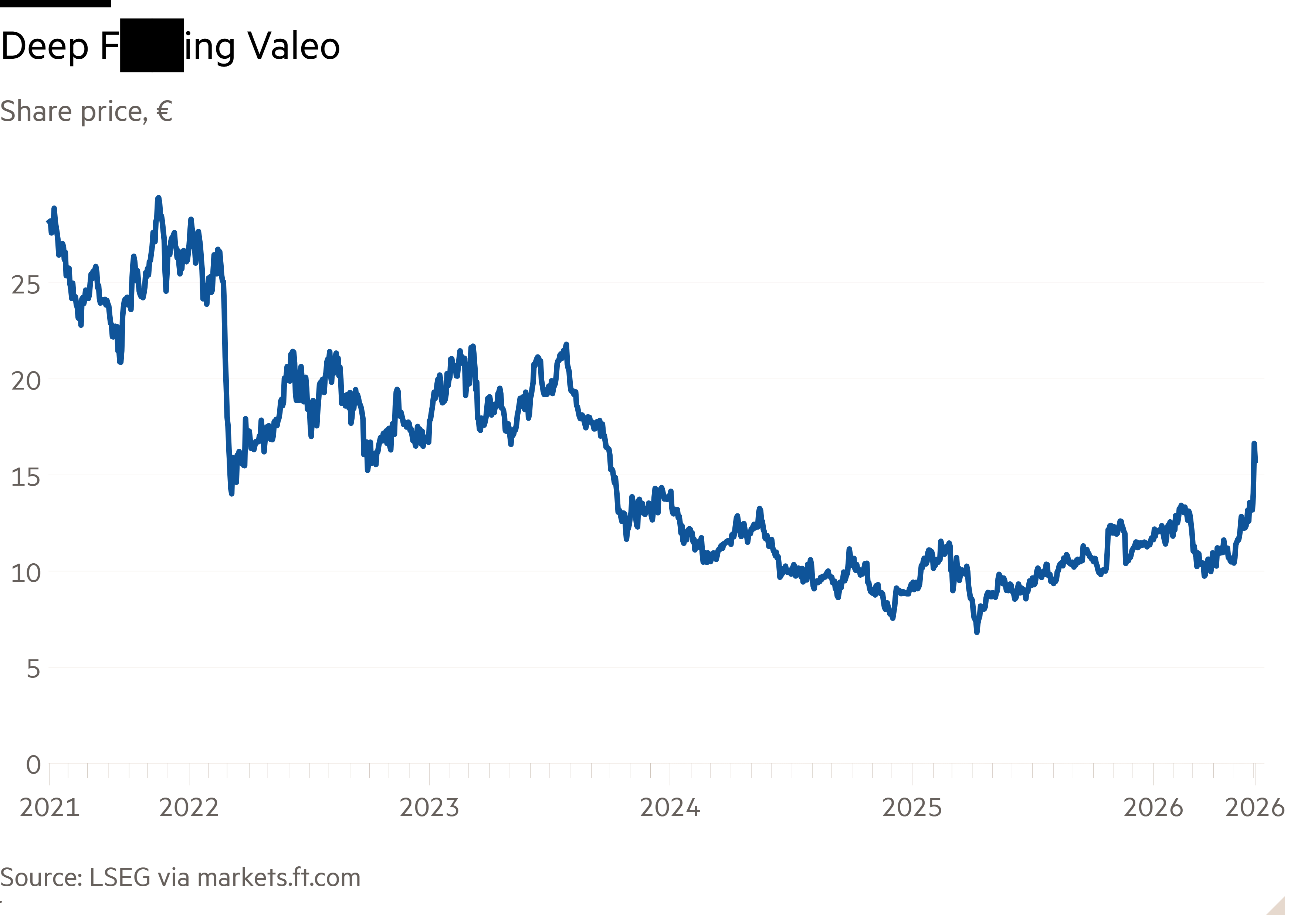

For example, Valeo. It’s a French supplier of auto parts. Supplying auto parts is a pretty miserable game right now — what with chip shortages and tariff threats, manufacturing moving to China, stalled US electrification, European overproduction, and new car sales nearly everywhere in long-term decline — so it’s understandable that Valeo management would rather be doing something else. What they’d rather be doing is AI.

Valeo shares printed their biggest gain in forever this week, prompted by nothing other than a scheduled appearance at a JPMorgan European autos conference to deliver a presentation that hardly mentioned autos. AI infrastructure is now the thing. One broker called it an “anything but autos” strategy.

It’s not our intention to dunk a pivot. Maybe Valeo’s specialities are transferable? Auto engines and AI data centres both use liquid cooling. Power management systems don’t have to be mobile to be useful. Robots of all shapes need sensors and widgets. Humanoids are, to an assembly line worker, just cars with legs.

The worry is that (aside from one battery storage contract Valeo won in February) the AI business lines are all pre-revenue. They’re moonshots.

We should also note a short squeeze. Some investors had loaned out their shares to coincide with Valeo’s ex-dividend date (the cut-off date for receiving the next dividend) at the end of May, so short interest was still a bit higher than usual. When the stock rose, short sellers rushed to buy shares back, helping push the price up. So it’s not just investors barking like seals at any mention of AI, though there’s undoubtedly a bit of that.

{kind=link}

Our point is only that we’ve been here before. In 103 years of operation, Valeo sold nothing other than auto parts. Now, suddenly, it’s a concept stock. It’s exciting when old-economy companies can add a billion euros by value on a hypothesis, but it rarely works out well for everyone.

A week on Alphaville

○ Golf club memberships, clothing allowances and relocation expenses all feature in this year’s Proxies, a celebration of substantial corporate perks.

○ We just don’t understand private credit, says Apollo CEO Marc Rowan, who likes to claim it’s a $40tn market of which only $2tn is below investment grade. Toby Nangle lists all the ways in which he’s probably wrong.

○ What’s been going into the ever-growing “other currencies” category of the IMF’s tally of central bank reserves? Here’s one candidate.

○ This will be an absolutely mammoth year for IPOs. Probably.

○ With SpaceX not being offered automatic entry into the S&P 500, passive investing is getting a bit more active.

○ UK GDP readings might be more reliable if you seasonally adjust the data twice.

○ What do you call an activist investor that doesn’t do activism? We call them an activist investor.

○ Rising star of the US Democratic left, and self-described class traitor, Saikat Chakrabarti is extremely rich. Sujeet Indap breaks down his investment portfolio.

○ Here’s your chance to buy a collection of supercars previously owned by Paresh Raja, founder of collapsed bridge lender MFS.

○ Spain will beat Argentina in the World Cup Final, England will be knocked out by Brazil in the quarters, and the US will defeat Iran early in the knock-out rounds, according to a Goldman Sachs quant model.

○ Because of the unique way Alphaville is funded, we can make a vibe-coded browser game about an ONS inflation basket item and release a range of themed merch without ever having to explain ourselves.

Promotional interlude

Registration is open for the FT’s new stock-picking contest. It has daily trading, mini leaderboards and a £1000 cash prize. Give it a go, why not?

Best of Further Reading

○ Ancient, Archaic and Classical histories of weather pricing, by Umit Dhuga.

○ Hanno Lustig’s The Two Cents newsletter considers America’s cap table.

○ The Atlantic considers the downsides of boom times in Spain.

○ How philanthropy can be the cornerstone of an industrial strategy for civil society, by Polly MacKenzie.

○ Reminisces of former Meta in-house pastry chef Titty Boobowitz (not her real name).

Chart blast

○ John Burn-Murdoch’s latest is on AI productivity, and how making stuff easier to make neither makes stuff better nor makes better stuff.

○ Martin Wolf, the FT’s own non-artificial superintelligence, seeks to make sense of AI.

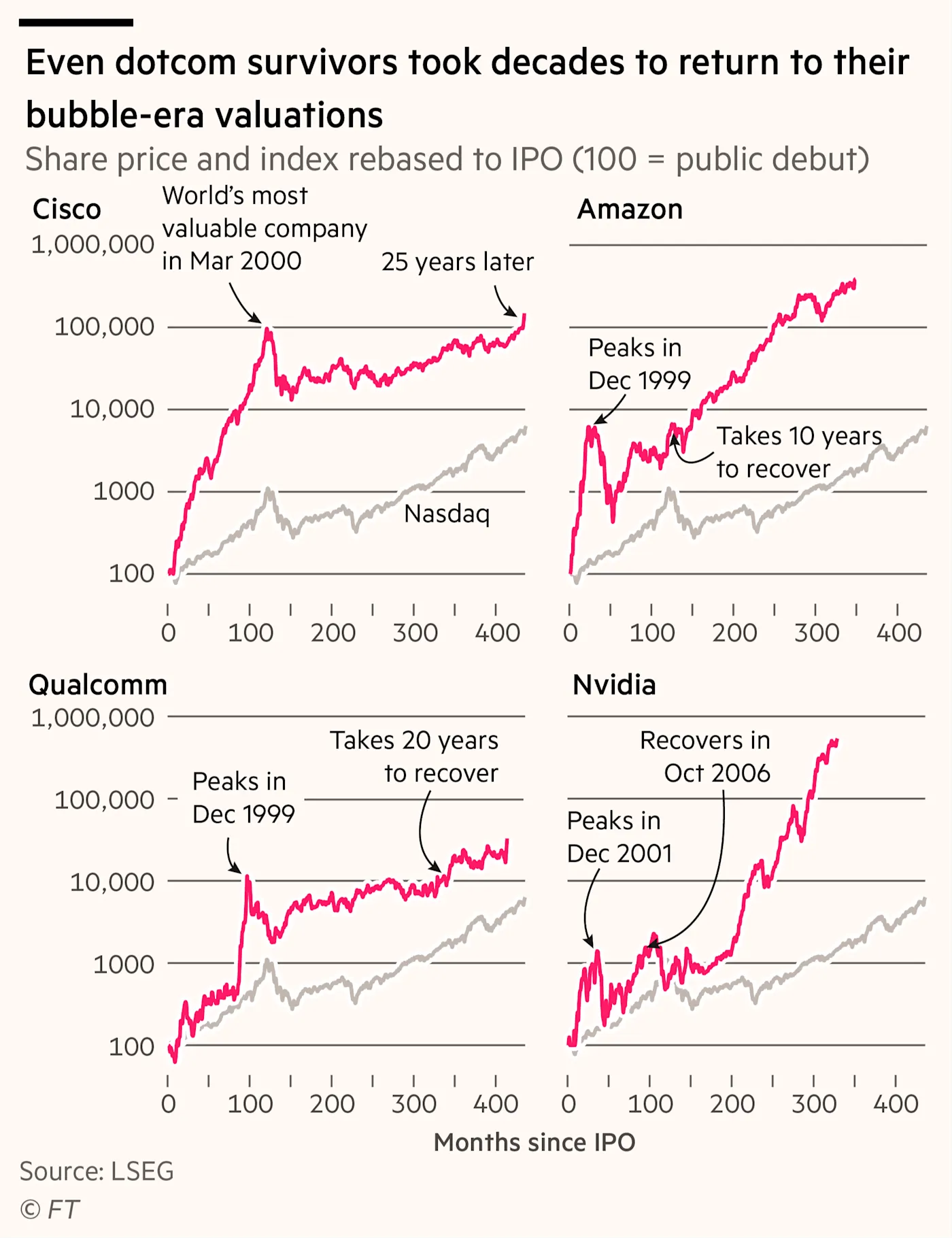

○ After a crash, even for the winners, it can be a long way back.

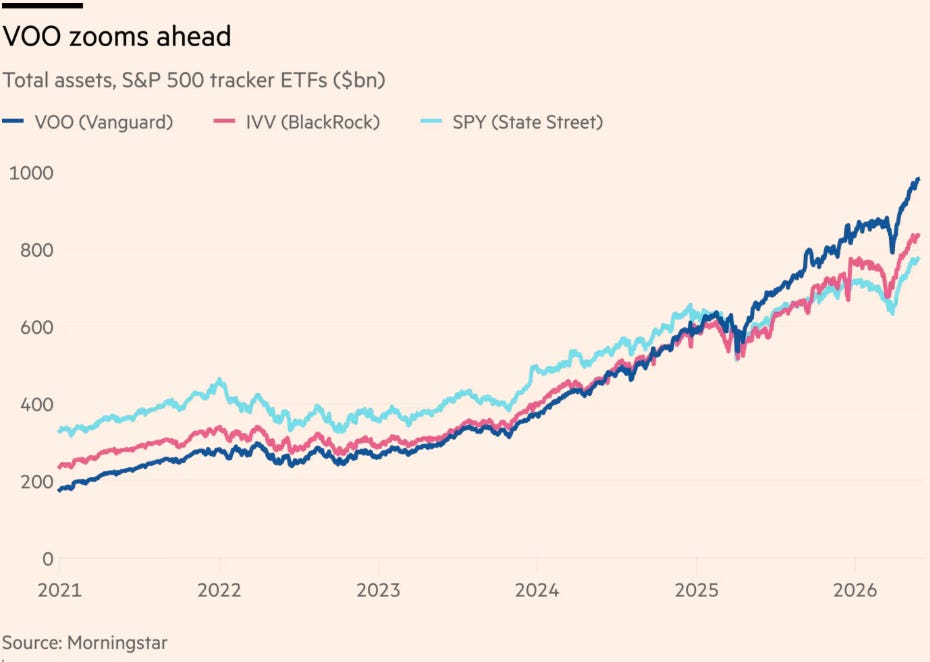

○ Vanguard’s S&P 500 tracker is the first ETF to hit $1tn of assets under (minimal) management.

The Valeo case raises a question the piece circles without quite landing: at what point does a sector label become analytically useless? An auto parts company with pre-revenue AI moonshots is still classified as Consumer Discretionary or Industrials, depending on the index. The allocator running a sector tilt is holding something the label no longer describes.

The Apollo private credit observation is the sharper one. Rowan's $40 trillion market claim with $2 trillion below investment grade is the kind of framing that makes the asset class look orderly from the outside while concentrating the analytical work entirely on what sits in the other $38 trillion. That is either reassuring or terrifying, depending on your prior.

Humanoids are just cars with legs is the best sentence written about AI industrials this week.

The comparison between 2000 and now has a probability layer worth making explicit. In 2000 the market was not wrong that the internet would reshape business. It was wrong about the hit rate, pricing every web-adjacent pivot as if it had a one-in-three chance of being Amazon when the base rate was closer to one in fifty.

The same structure sits inside the Valeo move. The market is buying an option on an AI pivot, which is a rational thing to price. The question is what implied probability it has assigned to a 103-year-old auto-parts supplier building meaningful AI revenue before the narrative window closes. One battery storage contract and a set of conference slides about liquid cooling probably warrants something in the low single digits. The stock moved as if it were multiples of that, and the short squeeze made the mechanical look informational.

That is the part of the cycle the dot-com parallel should warn about. The pivots that worked, Amazon and Nvidia, looked identical to the ones that failed at the moment of the announcement. The market could not tell them apart either, but it priced the whole portfolio as if the hit rate were high. The error was in the portfolio implied probability, not in buying optionality on the narrative.