Not the future. Don't talk about the future.

Plus: Alphaville's own analyst note on SpaceX, the end of reading, forecasting recessions, bubble earnings

Sure, ceding the future to a handful of megacaps controlling godtech might mean there are going to be a few losers. We’ve already had a glimpse of who the first against the wall could be, and what this might mean for incautiously diversified high yield credit investors.

But technological progress that boosts productivity and utility is good! It’s supposed to give us time and resources to do more stuff we enjoy.

Or maybe it allows us to do more of the annoying stuff we currently pay for all by ourselves. As Oxford economist Carl Frey wrote in MainFT last month:

The sociologist Jonathan Gershuny identified this pattern in 1978. Modern economies, he argued, were not heading towards a service utopia but a self-service economy in which households would absorb the work themselves. The washing machine illustrates this: it did not automate the laundress’s job — it gave customers the means to do without her.

Lawyers, tax accountants and electricians are expensive. And while you might not trust all this stuff to ChatGPT today, maybe you will as frontier models improve.

Legal/ tax/ horrifying death risks aside, any drawbacks?

When work shifts to the consumer, it vanishes from the economy that statisticians measure. A company that replaces a billing department with a chatbot interface records lower costs and higher output per worker. The national accounts register a productivity gain. But the hours that patients spend decoding their own tests appear nowhere — not in labour statistics, not in GDP. As AI self-service expands into professional domains, this blind spot will grow.

OK. But should we care if AI shrinks the market economy in the process of maximising our utility (pretending for a moment that outsourcing hard thinking to a bot doesn’t lead to an atrophy of the mind)? Let’s braindoodle this out.

Sci-fi writers have long imagined how post-scarcity economics might play out. And legions of robot butlers and AI bookkeepers could be what we need to usher in the kind of reputation-based economy that forms the backbone of Trekonomics. Admittedly, it’s not entirely clear that integrity is really becoming more highly prized.

There are darker visions too. And it’s not that hard to imagine an extrapolation that takes us to an Elysium scenario along with a reversion to the kind of social structures last seen in the time of the pharaohs.

Too much doodle. Let’s stick to more prosaic matters that sit more in our lane.

Governments’ income rely almost entirely on taxing flows in the market economy. And so if AI really really delivers — boosting our utility and beaming us up into a post-scarcity world (the happy version) — those market economy flows could start to dry up.

But even if legions of self-assembling AI-robots take over the humdrum government work of processing tax returns, teaching kids, enforcing law, and fighting wars —releasing millions of workers to spend more time with their utility, and so slashing the market cost of government — legacy debt will still need to be serviced. This means taxing an ever diminishing flow of market activity at ever-higher rates.

And so maybe it makes sense for both the left and the right in America to champion/ normalise their form of wealth tax.

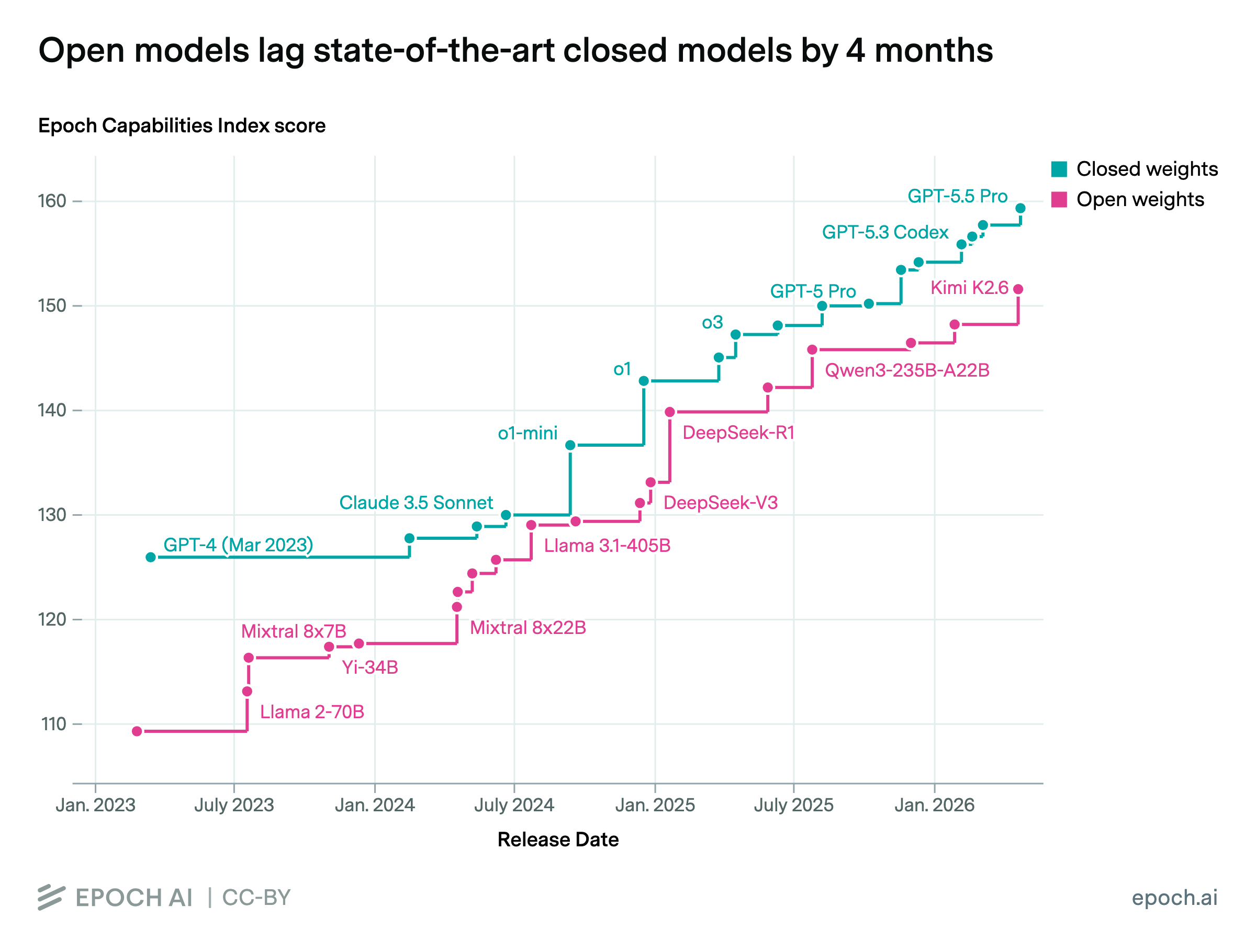

Still, while we’re doodling, it’s worth pondering once more whether the economics of making frontier models and monetising them before free-to-download open-weight versions catch up will really play out. According to Epoch AI we’re talking around four months of lead time:

Four months is not nothing, and the market is currently saying the firms at the frontier are big enough to bear capital taxes being mooted. Then again, the potential necessity for capital taxes is all predicated on the idea that governments retain an interest in keeping money around in the post-scarcity world at all.

Of course, speculating about the future is a mug’s game, especially when it comes to technology.

Geoff Hinton — the Nobel prize laureate so-called godfather of AI — was so confident about the technological strides being made that he made a public call for radiologists to stop being trained back in 2016, forecasting that they’d be made redundant by deep learning in five, maybe ten years.

Ten years on there are ten per cent more radiologists in America than there were then. But even this growth in personnel hasn’t kept up with demand, and the shortage has seen their average salary leap to around $680k, with senior radiologists earning potentially much much more.

Carl Frey himself shot to fame in 2013 as co-author of a widely-cited paper predicting that 47 per cent of total US employment was at risk of automation over the next two decades. Their forecast might still come true, but 13 years in it’s looking like a harder and harder ask, even turbo-charged by the AI revolution.

These two guys are far smarter than us. And seeing how off their forecasts have turned out leads us away from putting any weight on our own.

Instead we’ll continue to marvel at the ever-fascinating evolution of the sociology of power through the lens of reified money-weighted expectations. Aka, we’ll be watching the prices of stocks and bonds:

And right now the market is happy to pay 10 or 20 times sales for the handful of companies they reckon will get to own, or at least control, the future. We reserve the right to point and laugh if this turns out to be epically wrong.

In case you hadn’t already guessed, Bryce is off today. So don’t blame him for this one.

A week on Alphaville

○ The space bit of SpaceX is worth only $8 a share, says Morgan Stanley. Target price $300. And RayJay pops a $800 price target on the stock.

○ Alphaville LLC initiates coverage of SpaceX with Buy recommendation. Target price ∞.

○ A deep dive into the unsung daddy of primary capital markets — how the corporate bond sausage is made.

○ Adam Shaw takes a look at how concentrated the semis market really is.

○ What happens if a bubble valuation is applied to bubble earnings? Bubble-squared™.

○ Ryan Avent writes an obituary for secular stagnation.

○ Worrywarts were gathering last year as European banks were getting stuck into synthetic risk transfers. What happened next?

○ The Bank of England continues to sell long-dated gilts. Should they?

○ Remember how all the stock market gains happened between the close and the open? Robin dissects the death of overnight drift.

○ A quantitative take on Warsh’s minute minutes.

○ The UK turns out actually to be a pretty good international financial service centre, thank you very much.

○ Louis continues his public audition for the role of National Statistician role at the ONS.

○ Allianz makes a punchy doomstery metaphor about the role of private credit today.

○ Soumaya’s Economics Show guest reckons forecasting recessions is pretty much impossible.

○ CLSA share some ‘interesting’ views on who started a bunch of wars.

Best of Further Reading

○ Is the AI boom more like a tech bubble or a real estate bubble? Groundbreaker examines the second derivative, arguing that it’s the only way to understand the AI boom

○ On its semiquincentennial, The Grim Historian asks whether America has crossed the Asshole Threshold?

○ Meanwhile, Arcadian Asset Management uses the occasion to look back to America’s first bubble.

○ Finally, The Atlantic reckons the end of reading is almost upon us, and with it the capacity for critical thinking. Sigh.

Chart blast

Martin Wolf takes a look at the future of liberal democracy around the world, and reckons that the future is bleak. And he wonders whether the huge rise in the concentration of wealth of the top 0.00001% of Americans is just getting started.

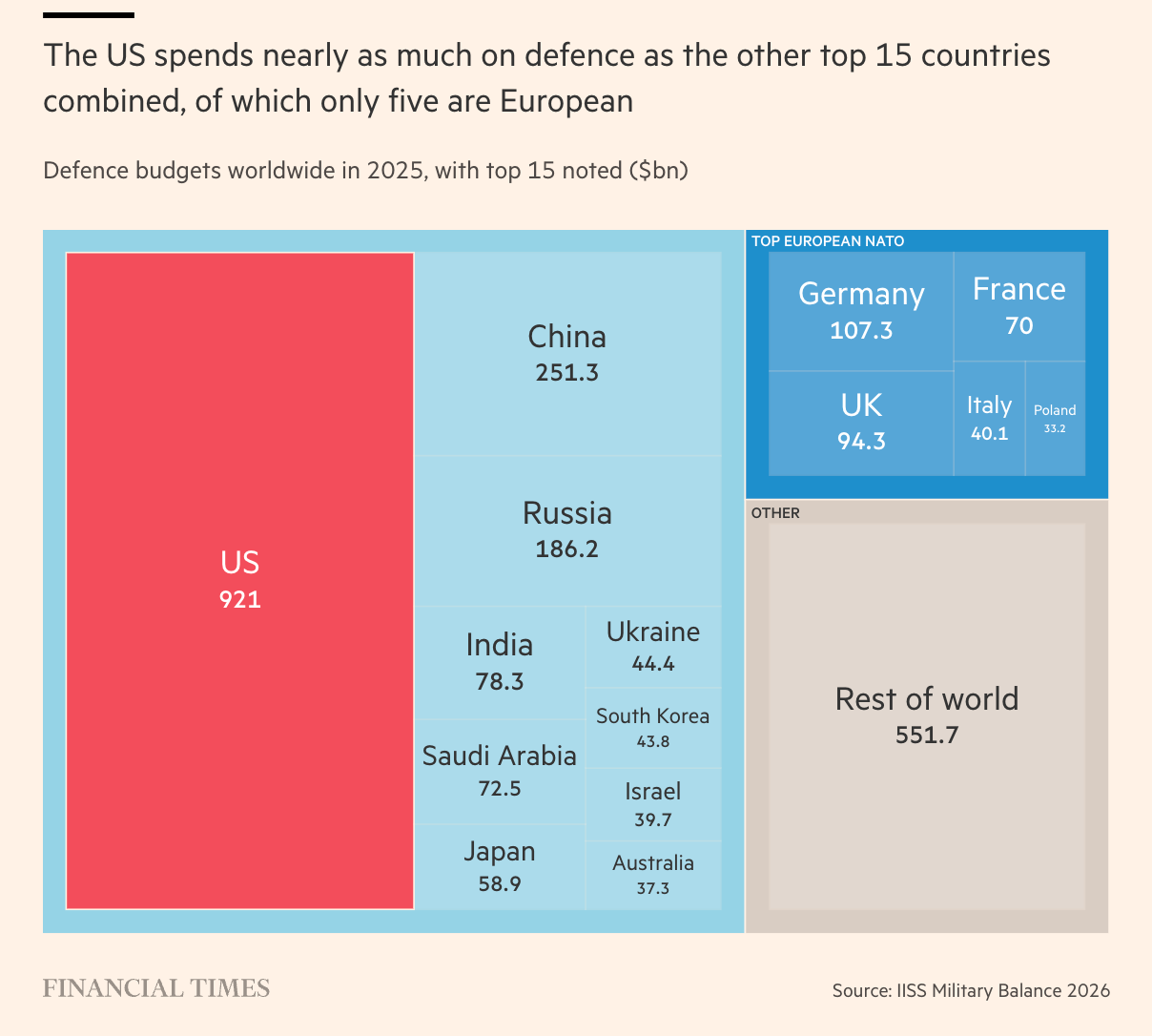

Ben Hall, Charles Clover and Henry Foy wonder how Europe would fight without America. Defence budgets are on the rise, but with America spending as much as the other top fifteen countries combined, are they rising enough?

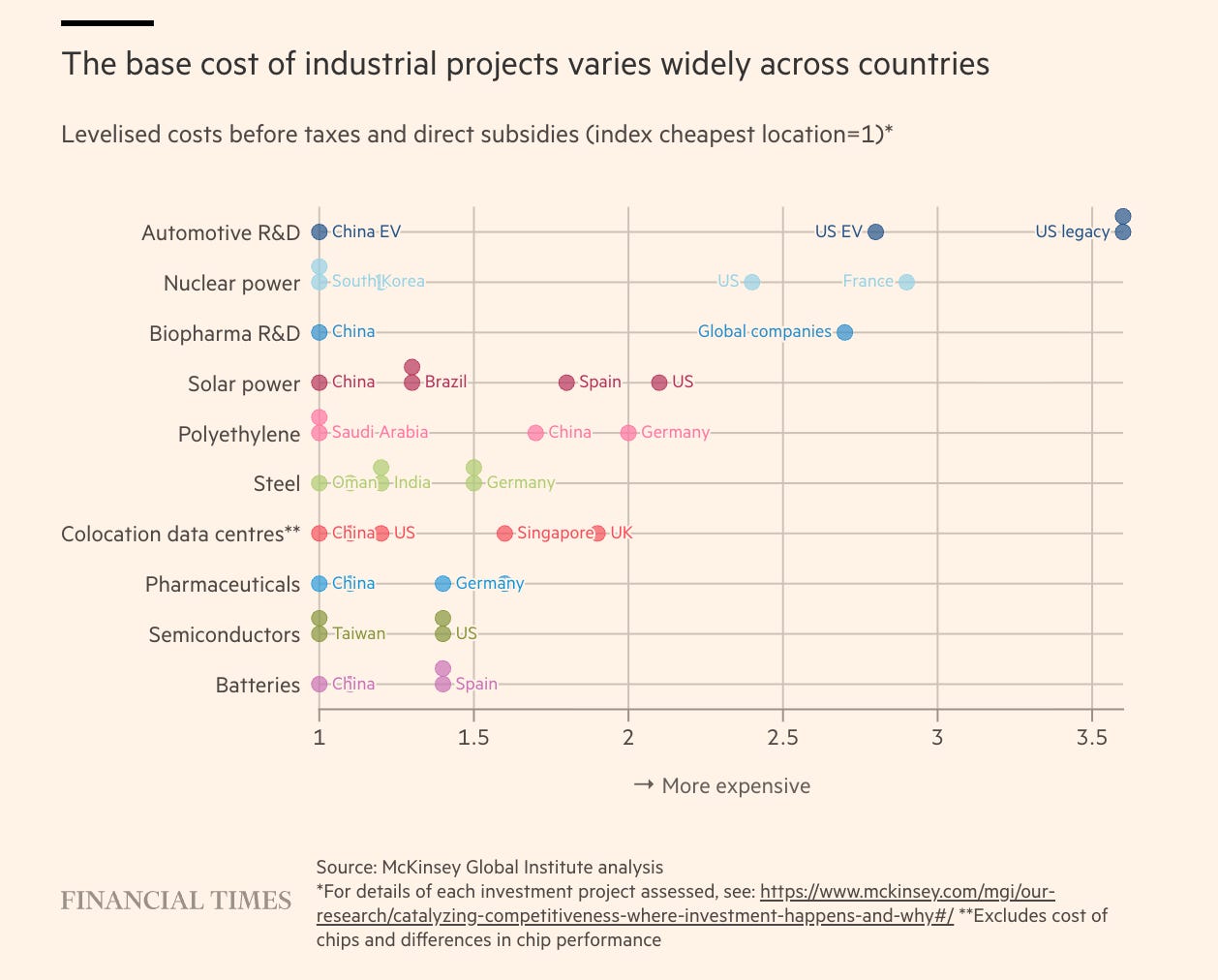

Tej Parikh reckons rich nations must unleash land, labour, energy and capital if they want economic growth, though finds European and US industrial set-up costs are 50 to 300 per cent higher in many sectors relative to the most competitive nations.

It’s interesting how quickly this starts to feel like an efficiency gain from the outside and a time transfer from the inside.

As more work moves onto the end user, the system records higher productivity and lower costs, while the actual effort hasn’t disappeared - it has simply moved to a place that isn’t counted. Over time that creates a subtle gap between what looks more efficient and what actually requires more input.

That gap is easy to overlook at first, but it quietly reshapes how value is perceived and priced.

Re: When work shifts to the consumer

Now there is a word for it!!!

Enshittification