It's quiet. Too quiet

Plus: tariff wars, sovereign defaults, private credit, Chinese cars, protein shakes, gig work, AI slop, and instant coffee

London Pub quiz

May 7. Team sign-up is now open. Details here.

The rock that keeps tigers away

Bill Ackman’s odd, but he knows how to pitch a story. The garrulous manager of funds and opinions this week made a sort-of takeover offer for United Music Group at a hypothetical valuation using money he doesn't yet have, that levers a majority of shares he doesn’t intend to buy, in support of a restructuring plan aimed at making the shares he owns go up, even though he lacks the public support of the controlling shareholder who due to conflicting interests may prefer the shares to go down. That most media reports skipped all these details and put a big dollar number above a picture of Taylor Swift is an example of Ackman’s knack for framing.

Bill Ackman is in talks to launch a strategy that would make big bets on complacency in financial markets, in a bid to mimic the success of doomsday trades the billionaire investor made during the pandemic.

Ackman’s Pershing Square would use the fund to make “asymmetric” trades aimed at profiting by wagering against the prevailing narrative in markets, according to people familiar with the matter.

Complacency is the theme of the moment. To be bullish right now means choosing to disregard surging energy prices, the threat of a stagflationary shock, a Middle East ceasefire in which firing hasn’t ceased, a blockaded Strait of Hormuz, a private credit unwind and a White House incumbent who’s corroding American exceptionalism one tweet at a time.

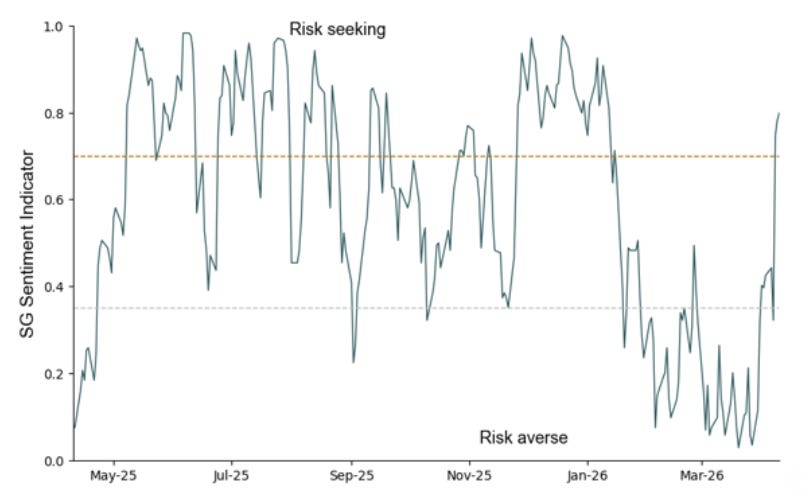

It sounds too much in combination, but, for the consensus, disregard is what’s happening. Stock benchmarks year-to-date are little changed or better. Bonds are doing nothing notable. The Vix volatility index is back to its February level below 20, while multi-asset measures like SocGen’s Sentiment Indicator have swung into the fill-your-boots zone:

Sensible people are saying sensible things. Here’s Robert Armstrong:

[T]he market should still be pricing in some chance of an oil-driven stagflationary snarl, even if that outcome became meaningfully less likely yesterday. But it is hard to find much sign that it is doing so.

And Gillian Tett:

[I]nvestors need to get better at imagining — and pricing — once-unimaginable disasters. This is hard. No business school teaches students how to model something like a presidential threat to wipe out a civilisation. And the success of the recent Taco trade will undoubtedly make many even more reluctant to do this. But the grim reality is that even if a ceasefire deal holds in Iran — a big “if” — peace looks elusive. […] So by all means celebrate that Taco moment and Buy The Dip. But buying a modicum of disaster insurance is also a wise bet.

Sage advice. The problem is how.

Professional money managers get to tweak discounts to match the prevailing mood, where credible apocalypse threats are worth an extra few basis points on top of their risk-free rate. Those with a more active approach can express their view through something thematic, like gold or soft commodities, or they can heft cash at credit default swaps while praying that things get worse before they’re insolvent. A third route is to seek protection with uncorrelated assets, such as life insurance policies or Counter-Strike skins or whatever.

All these options are difficult. They involve lots of work and cost lots in fees. The assets they’ll accumulate are relatively illiquid and carry all sorts of esoteric risks.

Wouldn’t it be easier to park some insurance money with a manager who did well in a previous crash? Even when their success is more easily explained by survivorship bias than foresight, the lack of good alternatives can make it an attractive pitch.

Hedge fund manager Boaz Weinstein already sells tail-risk funds based on his excellent record trading CDS through the Covid crisis, rather than a mediocre performance thereafter. Ackman — having a rough year, but similarly excellent with CDS during Covid — wants to do the same. For this moment, when uncertainties are depthless and markets seem ambivalent, it’s meeting a need.

Complacency protection is an itch that’s hard to scratch. Ackman promises a solution: sacrifice some percentage of your funds to his contrarian permanent capital vehicle and hope that you’ll never have to think of it again, with the bonus that he plans to sell you a Taylor Swift album to play while we’re waiting for the world to end.

Two weeks on Alphaville

○ No newsletter on Good Friday means it’s a bumper edition. Starting with a big animated timeline of global sovereign debt defaults.

○ Trump has built “a perpetual leverage machine with tariffs as the enforcement mechanism” that’s likely to outlast him, writes Sam Lowe.

○ US mortgage rates can fall if the idea of floating Fannie Mae and Freddie Mac gets canned, says Pimco.

○ European repo is very, very big.

○ Marshmallows can also be very, very big. What this means for their VAT treatment is, as usual, a descent into case-law madness.

○ THG, a UK-listed conglomerate we used to write about, is invested in finding out the far-from-straightforward VAT status of sports nutrition drinks.

○ Dogfooding — companies instructing bankers organising their IPO to use the products — happens more than it should. Craig Coben asks, has a line been crossed when the product is an AI chatbot owned by a rocket launcher?

○ Coben also riffs on Strategy’s use of AI slop video to promote STRC, its high-yield perpetual preferred instrument.

○ Introducing John M Fife, AI penny stock investor.

○ Some pretty chord diagrams showing how US household, government and business liabilities join up.

○ An update on the infighting at quant hedge fund Two Sigma.

○ Toby Nangle coins the Collateralised Whatever Obligation to help explain securitisation.

○ The current state of Middle East oil and gas infrastructure.

○ Why would we try to doxx Satoshi Nakamoto using text comparisons and that kind of stuff when it’s much easier to be snide about the efforts of others?

○ At what gold price does Tether’s USDT become balance-sheet insolvent?

○ Charting what’s happened to earnings estimates since Operation Epic Fury began.

Best of Further Reading

○ Via NBER, here’s a study of stock trading by US members of Congress that concludes they’re no better on average than the average schmuck.

○ Sakonnet Research (free registration) looks at how “poor regulation along with the federal government’s and Federal Reserve’s largesse” caused the private credit bubble.

○ Making gig work more easily accessible can reduce crime, says this paper summarised in VoxEU.

○ Works In Progress examines the creation of instant coffee.

○ Two bleak tales from hospitality: London Centric talks to the workers given unpaid front-of-house trial shifts that don’t appear to result in a job; and The Bureau of Investigative Journalism collaborates with Vittles to seek to hold Antipodea, a brunch chain, to account for ignoring employment tribunal rulings.

Chart blast

○ As a net energy importer that’s overweight industrials, transporters and consumer products makers, Europe’s an obvious short in an energy shock.

○ As Wednesday’s ceasefire relief rally shows, what’s obvious isn’t always profitable.

○ Big private credit funds in aggregate honoured just over half of the first-quarter redemption requests they received.

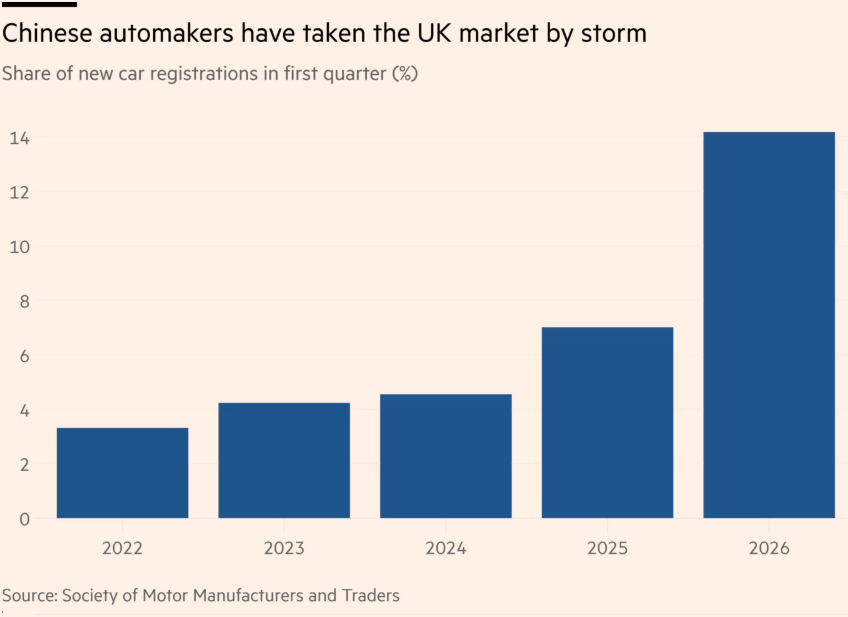

○ Chinese marques like Jaecoo and Omoda are rapidly making inroads into the UK auto market, while in the US, there’s a surge in sales of used electric vehicles.

Really should've done the private credit redemption chart in percent terms, rather than absolute.

The deepest problem with "buy disaster insurance" isn't cost — it's that the largest risks on that list are structurally unhedgeable. Private credit doesn't trade on exchanges. You can't buy puts on it. There's no VIX equivalent for $1.7 trillion in illiquid direct lending. The instruments available for tail hedging — equity puts, CDS, VIX calls — protect against the risks markets can already see and price. But the gates quietly going up at https://thesynthesis.ai/journal/the-cash-position.html suggest the real fragility lives in markets where no insurance product exists at all. Ackman's 2020 trade worked because credit default swaps existed for what he wanted to hedge. The next dislocation may originate somewhere the options chain doesn't reach.