Free lunch is cancelled

Plus: Chinese stock markets, Omani oil, Australian gas, American minesweepers, and Japanese vending machines

Forty to 60 per cent of the time, it works every time

If your reaction to the news last month that the US and Israel had begun airstrikes against Iran was to buy Fartcoin, congratulations, you win. Nearly everyone else lost.

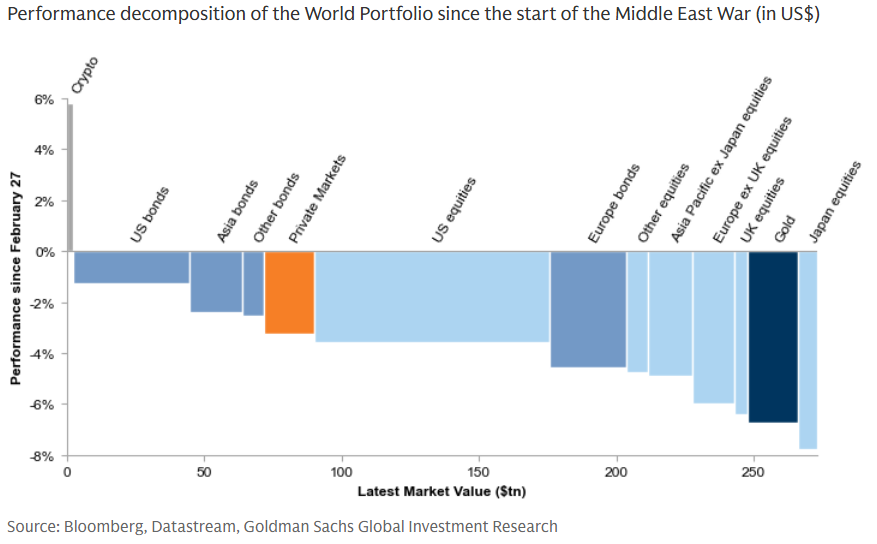

According to Goldman Sachs calculations, crypto is the only investable asset class to rise in value since the war started. Between then and Thursday morning, the value of global assets had fallen by $11tn.

Eleven trillion dollars sounds a lot but isn’t particularly. GS’s everything index tracks about $300tn in global assets, so it’s only a 4 per cent drawdown. That’s less than half a Liberation Day, and barely a fifth of a Covid:

More notable than the depth of drawdown is the breadth. Oil has kicked the chair out from under all the stuff the average investor has been favouring over the past year, like old-economy European stocks and dollar diversifiers. Equities and bonds have fallen together as markets seek to price in an inflationary shock of unguessable size and scope. Rising real yields eroded the defensiveness of defensives. Going by what the average punter can trade, that only really leaves cash and (not investment advice!) crypto.

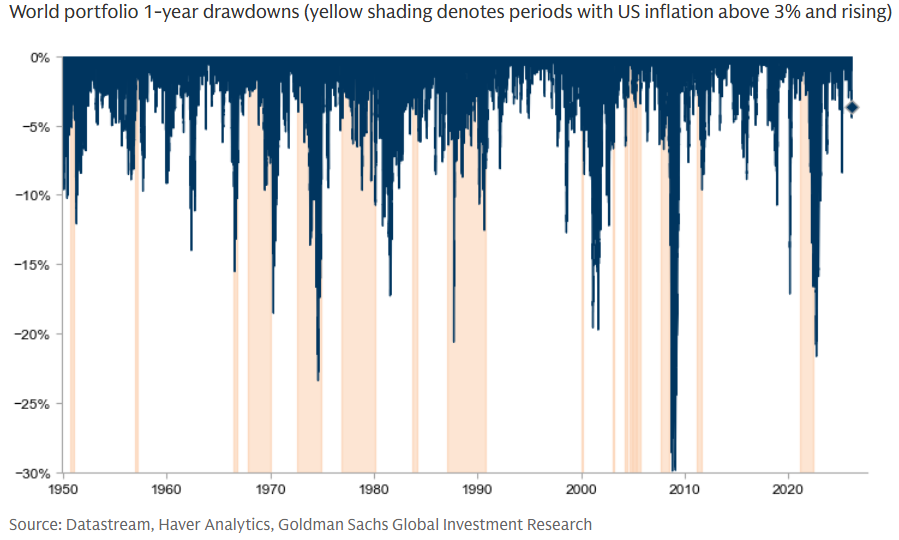

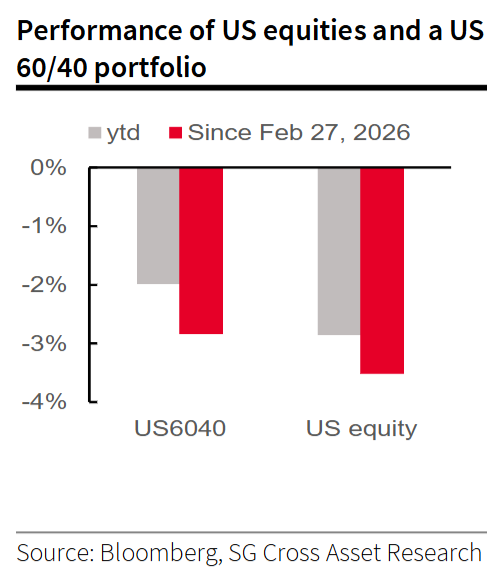

The sound you may hear is of financial commentators refreshing their obituaries for the 60/40 portfolio. A strategy of using bonds to cushion equity volatility has been declared dead every other month since the pandemic, so they have plenty of archive material:

Stock and bond returns tend to correlate whenever inflation is sticky above 2.5 per cent. Some version of this rule is now widely accepted, the solution being to add to the mix things like commodities, real estate, art, whatever. It’s fair advice. Buying a Bored Ape NFT probably won't do much for your Sharpe ratio but, for those of us not blessed with foresight, any type of portfolio diversification is going to be better than none. So long as the assets are not perfectly correlated, their average volatility should be reduced.

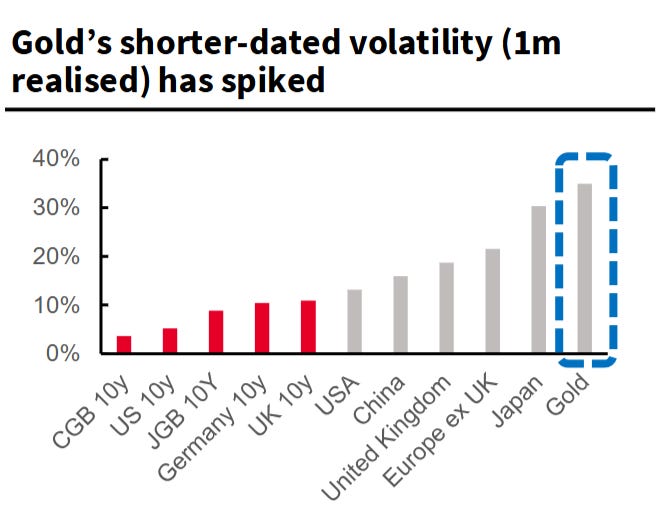

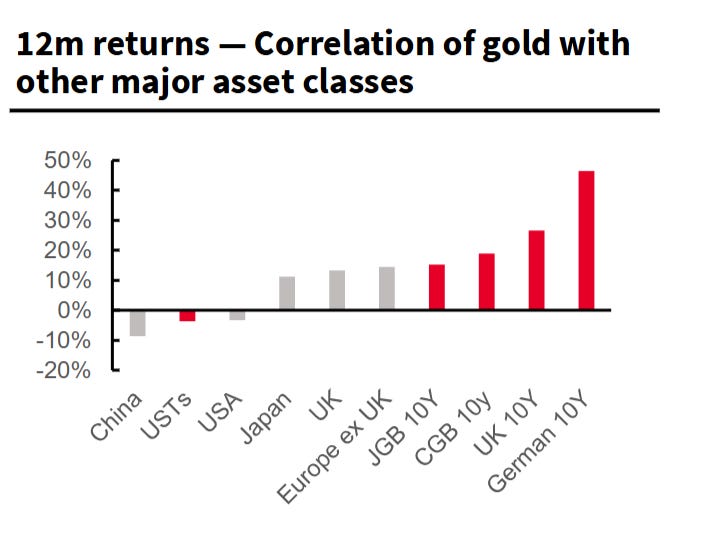

What’s unfortunate is that things have a habit of happening all at once, and “could be worse” won’t pay for many carefree retirements. Gold, for example, would normally be the safe option when bombs are falling. But dollar avoidance and the debasement trade earlier in the year turned gold into a meme. Charts via SocGen:

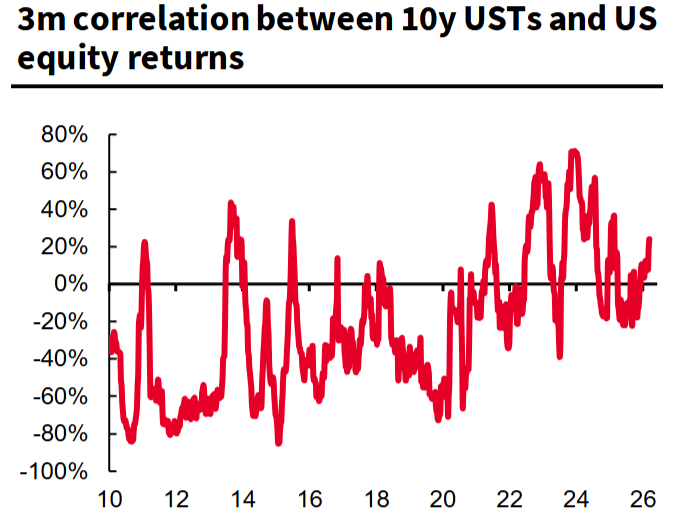

US Treasuries? Nope. They’ve been correlated with risk assets more often than not this decade so, while yields are rising and interest rate expectations are being repriced, the protection they offer is minimal:

Real estate? AI bubble.

Private credit? Ha. It’s never smart to ride into battle on a cockroach.

What’s the solution? No idea. Lots of smart people have been proposing improvements to modern portfolio theory, such as sausage-slicing how asset correlations are measured, while other types of people have been loading up on shitcoins. It’s the latter group who are out in front. The only conclusion to take from all of the above is that investing is hard.

A week on Alphaville

○ Chinese stock market returns are rubbish because Chinese companies have routinely diluted their investors by stealth.

○ S&P Dow Jones Indices is considering fast-tracking SpaceX into the S&P 500 because Elon wants exit liquidity, so screw you, ETF investors.

○ The US Office of Financial Research had a go at measuring the size of counterparty exposures to private credit.

○ Deutsche Bank reported year-end private credit exposures and, unfortunately for Deutsche Bank, it was found to be Deutsche Bank.

○ There are many markets for oil and, while benchmark Brent and WTI have been fairly subdued, a lot of the other ones are not.

○ Drawing down the US Strategic Petroleum Reserve won’t add that much to oil supply, but might cause some salt caverns to collapse.

○ A fragile peace is declared in the Bank of England’s Monetary Policy Committee.

○ Seven months after her appointment, Meg Ryan (not that one) is no longer the SEC’s Director of the Division of Enforcement.

○ Warner Brothers Discovery received and rejected a takeover proposal from a mystery Singapore-based firm that appears to be run by a former Raffles City Rotary Club president who has business interests in Cyprus.

○ Business is good for war machines, Eurostat’s European manufacturing data shows.

○ The British public voluntarily donated £1.7mn to the UK Debt Management Office last financial year, which is both quite a lot and not very much.

○ A brokerage with links to the Trump family that’s under investigation for allegedly assisting organised crime networks is giving the impression of playing regulatory brinksmanship.

○ RBC Capital Markets analysts looked at US biotech M&A rumours over recent and concluded that it’s best to trade on the ones the FT publishes, which is nice.

Best of further reading

○ Hendrik Bessembinder has a new paper on 100 years in the US stock markets.

○ Government bonds do badly on average through extreme events like war and pandemics, says this paper on CEPR.

○ For Foreign Policy Research Institute, Emma Salisbury on why the US saw naval minesweeping as “unglamorous, low-priority, and someone else’s problem”. (Have a go yourself.)

○ The oil price shock is causing big problems for Australia, writes Alex Turnbull.

○ Les Barclays of This Is Not Investment Advice looks into the “collateralised chip obligations” paying for the great AI buildout.

○ Polymarket degens have been sending death threats to a Times of Israel journalist who refuses to change a story about a missile attack.

○ Lauren Leek pulls the data to map London’s latte line.

Chart blast

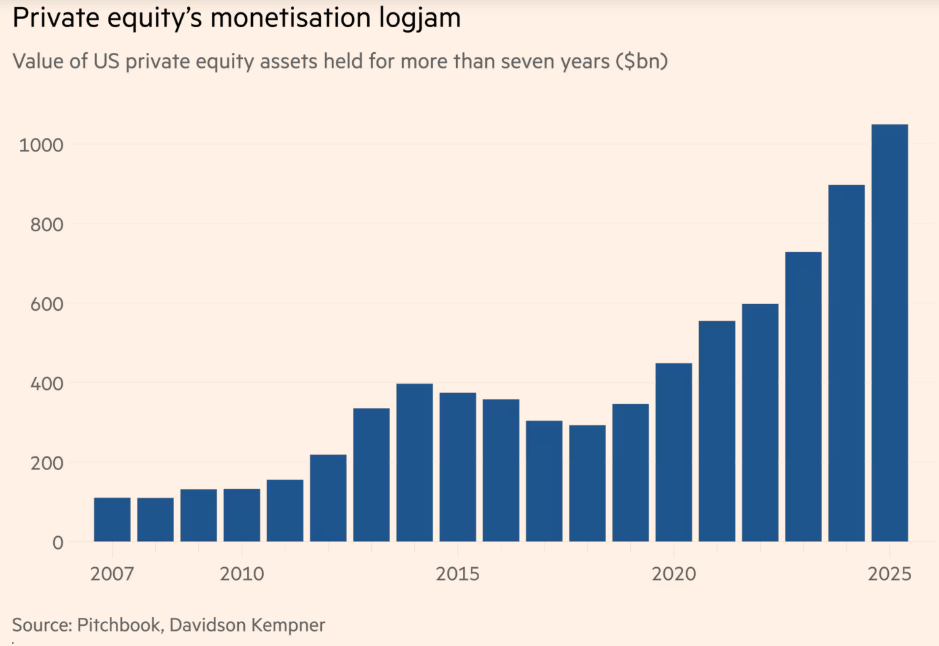

○ This week’s warning about the perilous state of private capital comes from Tony Yoseloff, managing partner at Davidson Kempner Capital Management.

○ TJ Maxx is huge and weird.

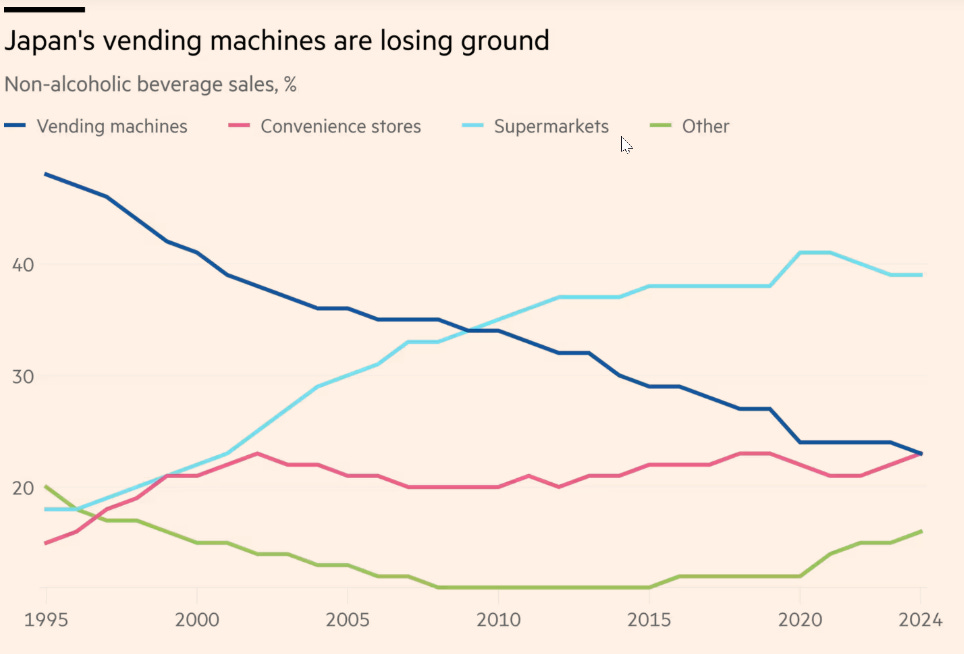

○ Japan’s vending machines are leaving service and not being replaced (news of which we accidentally put in a chart quiz earlier this month, having misread the publishing schedule).

Pretty sure oil is an investable asset class, and went higher since the war started.

Modern portfolio theory won’t hold if it’s money flowing out instead of money flowing in or flowing between bonds, equity, gold? Anyway. Short hedges in place. That’s what sits on the other side of long and does seem to be working just fine. Insurance.