Everything is stonks

Also: SpaceX, private credit spreads, lunar timeshare, faster massages, and young finance dudes in dapper suits

BTFD, Mr President

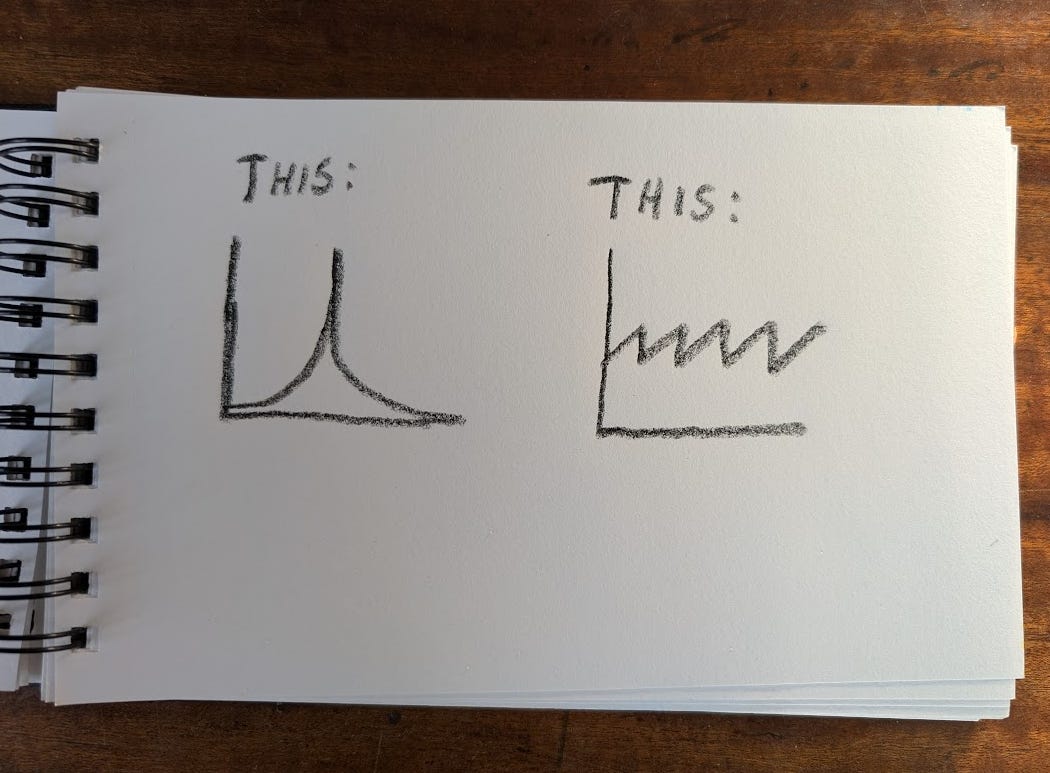

The two main types of financial market charts are this and this:

The one on the left tends to suggest a narrow momentum trade, such as silver futures. The one on the right tends to indicate a broader mean-reversion trade, such as the S&P 500. Between these extremes ought to be a diversity of pricing trends honed from rigorous analysis of all possible futures, each weighted by probability through dynamic price discovery.

At least that’s the theory. It’s not been working that way for a while.

Take, for example, Korean equities. The Kospi 200 index hit a record high on Tuesday, entered a technical bear market halfway through Wednesday, and set the floor for a new bull market early on Thursday. Even for a notoriously choppy index, that’s a lot:

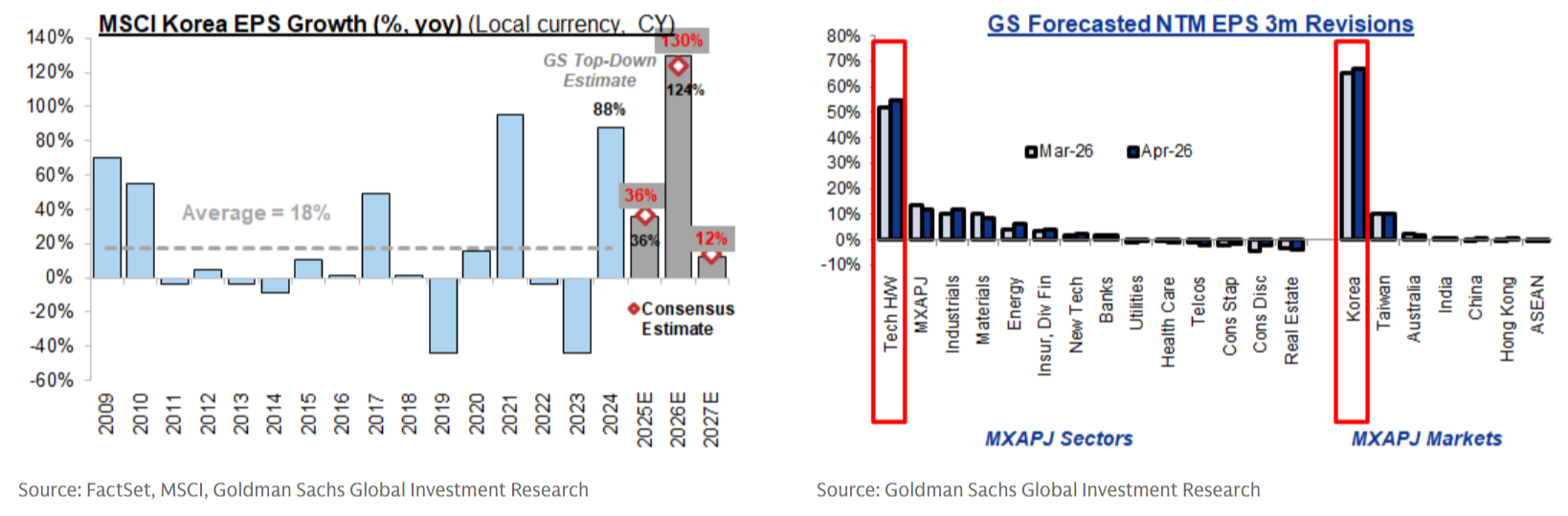

As tends to be the way, explanations abound. Korean stocks went up on AI-related chip shortages, fresh interest in heavy industry, a possible narrowing of conglomerate discounts, and K-Pop Demon Hunters. Korean company earnings will more than double in 2026, consensus expectations having shot higher in recent months. Jitters only surfaced when bombs started dropping 4,000 miles away.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

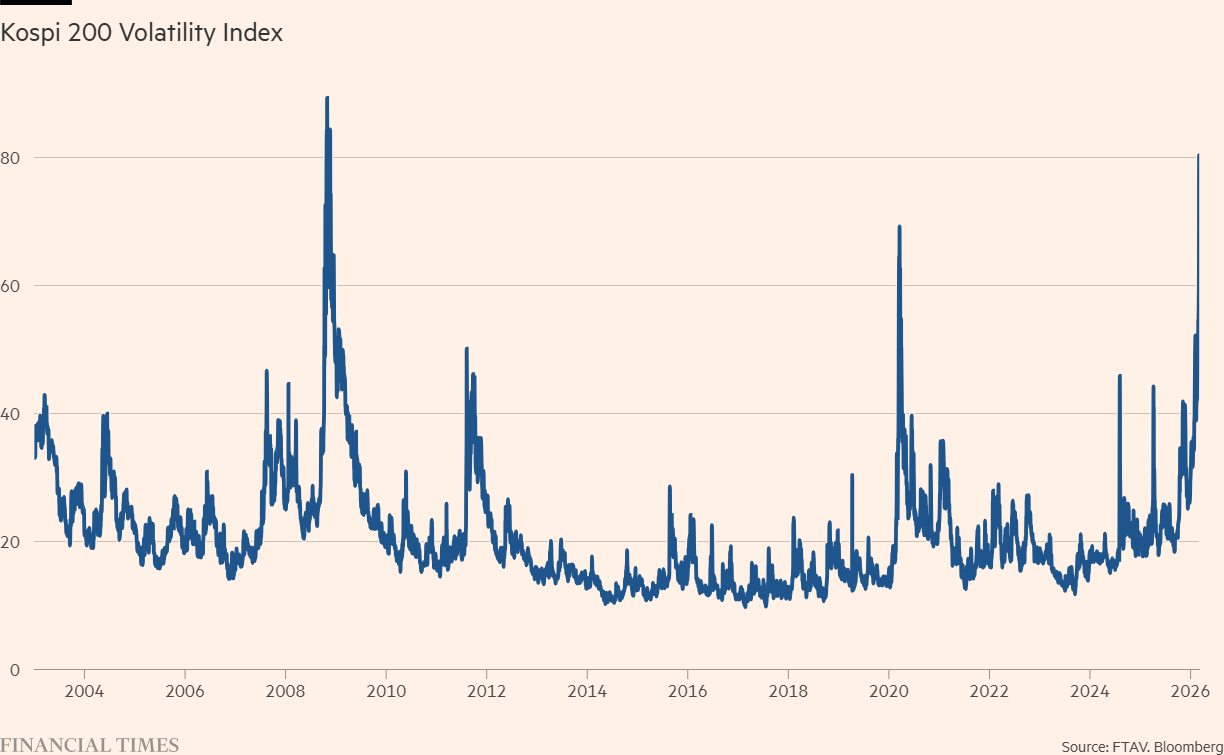

And with any rapid repricing comes volatility. Current uncertainty levels for Korean equities are rivalling the Great Financial Crisis, which is an odd thing to say about some memory chip supply bottlenecks and corporate stewardship code revisions, but there we are:

It’s mixed news for Korea’s punter army, who in recent years have been weaned off property investments and into stocks. President Lee Jae Myung this week activated a $68bn plunge protection fund to quell panic selling, having last week led by example and sold a rental apartment to buy ETFs.

“At the small downtown office of Mirae Asset Securities, scores of clients hurriedly lined up to get their money out,” reports Bloomberg:

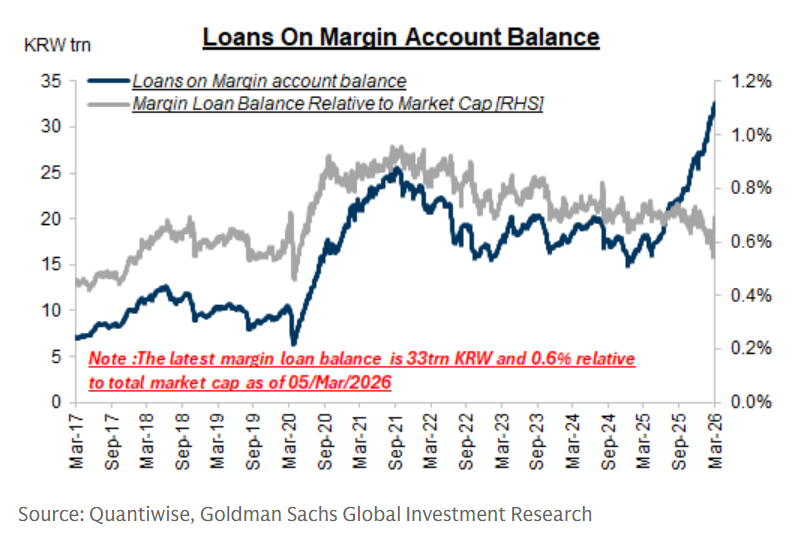

What the episode shows is just how fast a market dominated by leveraged, margin-fuelled bets and amped up by frenzied day traders can sour, exposing the risks of an investment culture that had come to treat borrowing as a sure thing to bigger gains.

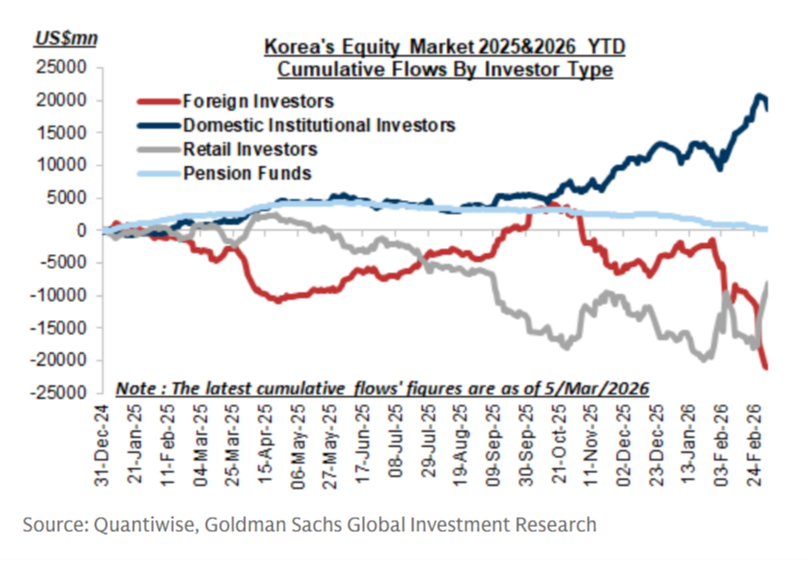

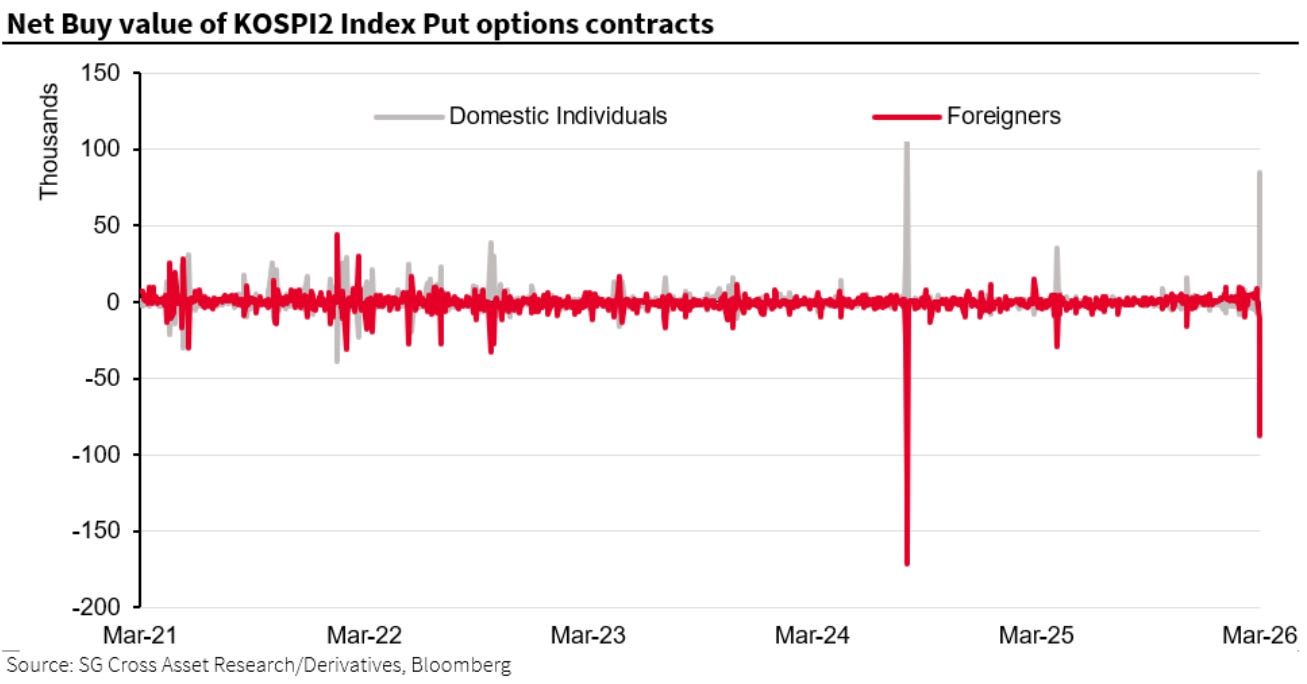

True, though it also shows the rapid flip-flop between greed and fear. A mania among Korea’s retail investors only really caught hold in February, and while their leverage levels are high in absolute terms, they’re unremarkable relative to market value. Some tourist capital will have been caught up into Korea’s recent rally, though risks can be overstated when retail and institutions are taking opposite sides of the bet:

{kind=link}

{kind=link}

All of which brings us back to the diagram at the top of the page. Powering the hand-crafted spike and sawtooth charts are two factors: momentum and mean reversion. In both cases, they’re amplified by retail and professionals taking opposite sides.

Last month’s AI disruption scare is a prime example. “Retail’s appetite to buy the dip has remained a dominant force in early-2026 flows,” says Citadel Securities, which reports net buying of US equities by individuals at nearly a five-year high.

This is an interesting stock market story: Are retail investors the ultimate value investors in the stock market? Does the constant retail buy-the-dip bid insulate the market against volatility?

Maybe it does until it doesn’t. There’s a dampening effect to having lots of retail money sloshing around, but add a product shortage or an inflation scare, and it remains a volatile accelerant. Volatility is suppressed until it’s not. You can’t choose which chart you’ll get. There’s no BTFD without YOLO and FUD.

A week on Alphaville

○ The SpaceX IPO is a monster.

○ One of the most popular publicly traded wrappers around SpaceX shares is in a bit of a spot.

○ Private credit spreads look tighter than you might’ve imagined.

○ Among active fund managers, Capital Group wants you to know it could be worse.

○ What will happen to oil prices?

○ Inflation worries are concentrated on the short end, with some transatlantic dispersion.

○ Barclays has gen-AI generating its AI analysis.

○ Lunar holiday home pricing. Yes, really.

Best of Further Reading

○ Svenska Dagbladet and Göteborgs-Posten investigate the data categorisation squads employed by Meta to snoop through its pervert glasses.

○ Private equity weakens companies in predictable ways at the cost of customers, clients and employees, says this University of Chicago Law Review study.

○ Hanno Lustig parallels joint debt issuance in the Eurozone with Alexander Hamilton’s America.

○ Not All Doom’s Arthur Snell revisits moron risk premiums.

○ Interview magazine asks New York finance dudes some fairly dull questions and gets some fairly dull answers.

Chart blast

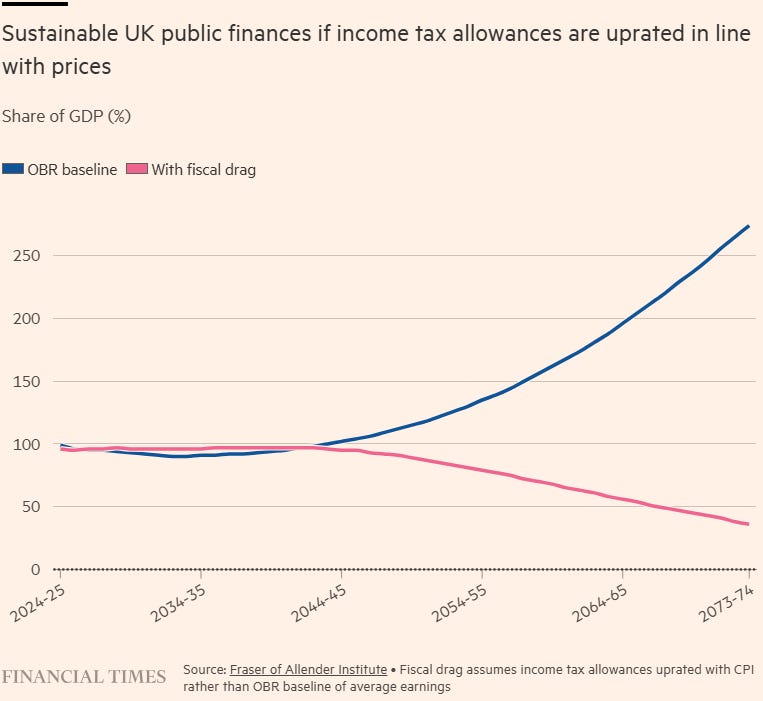

○ Chris Giles on the OBR’s charts of doom, and how they look a lot less alarming if income tax thresholds are assumed to rise with prices rather than wages.

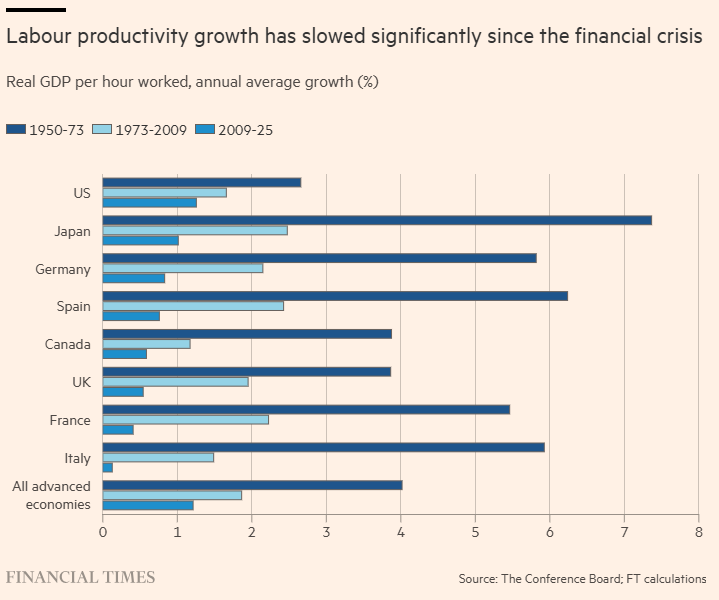

○ “We don’t want a massage more quickly, we don’t want to play golf and go for a leisurely hike more quickly”, says economist Claudia Goldin in this long read on why productivity stalls in economies with ageing populations.

○ Italy’s workforce is benefiting from political stability, strengthening GDP growth and an improvement in public finances; the UK, less so.

○ The apparent purpose of prediction markets continues to be to transfer money from people who don’t have inside information to those who do.

What have we missed? What did we get wrong? What can we do better next week? Let us know at alphaville@ft.com.