A Huge Ever Growing Pulsating IPO That Rules from the Centre of the Elonverse

Also: Libor redux, Russian banknotes, coppernose stablecoins, quantitative Aristotle, orbital antiperspirant, space strawberries, and selling out

Connect the dots, said Steve Jobs. “You can’t connect the dots looking forward; you can only connect them looking backwards. So you have to trust that the dots will somehow connect in your future.”

In the 50 years since Jobs co-founded Apple, its story has been told often. A glib summary might be that it fought a 30-year war for corporate desktops, lost, and pivoted the main business towards adding functions to MP3 players. To correctly anticipate any part of this from reading Apple’s flotation prospectus of 1980 would have had a person burned as a witch.

Then there’s Amazon. “Amazon.com is the leading online retailer of books,” its 1997 registration statement begins. “The Company offers more than 2.5 million titles, including most of the estimated 1.5 million English-language books believed to be in print, more than one million out-of-print titles believed likely to be in circulation and a smaller number of CDs, videotapes and audiotapes.” One solitary mention of servers (which accounted for nearly 60 per cent of Amazon’s operating profit last year) is in the context of its own potentially catching a virus.

Here’s another one, from 2004: “Google is not a conventional company. We do not intend to become one.” (Spoiler: lol!)

What about some spicier IPOs? Measured by trailing 12-month revenue, Akamai may be the most expensive big US float of the dot-com era, according to S&P Analysis. The web traffic manager is still recognisable as the one described in its 1999 IPO filing, broadly speaking. The challenge for any investor would have been to anticipate that the same business would be valued at more than $27bn in 2000, less than $78mn in 2002, and back to around $20bn again for much of the current decade.

-4ee317b1-9d47-4624-b93a-45b2b4c78cdc.png){kind=link}

{kind=link}

S&P’s list of expensive IPOs puts Webvan in second place. “We believe that our innovative business design is the first solution to adequately address the ‘last mile’ problem of e-commerce fulfilment,” reads the summary bumf for its $4.8bn float in November 1999. “The significant capital investment in our business system provides us with a competitive advantage compared to traditional supermarkets and other online grocers.” Nineteen months later, Webvan had become a dot-com bubble momento mori.

Then there’s SpaceX. Its route to market has been longer than any of the above. Burning private capital has already delivered us reusable rocket ships, sat-phones, and a race-bait website that might one day develop artificial superintelligence. Public life might add orbital data centres and planetary colonisation. Maybe there’s more reason than usual for paying attention to the 38 pages of risk factors in its S-1 filing. Maybe there’s more reason than usual to trust estimates stretching to 2045 that justify its $1.75tn valuation. Corporate survival usually means transmogrification, but, as a mature business with added moonshots, SpaceX might be different.

Does that mean SpaceX resembles what Amazon was in the mid 2000s, with the foundations for explosive revenue growth already built? Or is it more like Apple in the early 2000s, when its most valuable asset was a CEO who could create reality distortion fields? Is it more like Akamai in 1999, with products too immature to value, in pick-a-number total addressable markets, and with key-person risks that could never be anticipated? SpaceX is not going to flame out like Webvan, presumably, but after that, we’ve no idea. Neither do you. Neither does Elon Musk. Dots only connect when looking backwards.

A week on Alphaville

○ How to build a better way to rate rates.

○ Does a bitcoin sale mark the start of the end for Michael Saylor’s Strategy? Yes.

○ Benchmark huggers may need to put about $14bn into SpaceX.

○ A couple of links to Morningstar notes saying SpaceX would still be too expensive at half the price.

○ The UK retail portion of SpaceX’s share sale uses a newly introduced listings rule designed for start-ups and small growth companies.

○ XOVR, also known as the SpaceX ETF, is battening down the pre-IPO hatches.

○ Whatever else SpaceX is, it’s a spectacle.

○ Gresham’s Law as applied to stablecoins.

○ What Aristotle can teach us about AI-enabled quantitative investment. Yes, really.

○ Every slice of China’s bond market has now succumbed to Japanisation.

○ Growing strawberries in space is a costly business, it seems.

○ This link is provided with intention.

○ The daily grind must be rough at Starbucks.

○ With Tate & Lyle on the way out, we look at what’s left of the UK market's old guard.

○ All you’ll ever have to read about World Cup estimated macroeconomic impacts.

Best of Further Reading

○ Experimental History has a multifaceted read about pop music, consumerism, and the forgotten concept of selling out to the mainstream.

○ The story of “how antiperspirant fumes nearly got NASA to evacuate the space station”, from Mars for the Rest of Us.

○ We recognised a lot in this scream into the void from CityAM’s deputy comment editor about AI-assisted submissions.

○ It’s hard to pick others because this week’s links were nearly all great. Click through for each day’s dump, which includes bank laundry, iPhone distractions, taxing compute, screensavers, and horse cake.

Chart blast

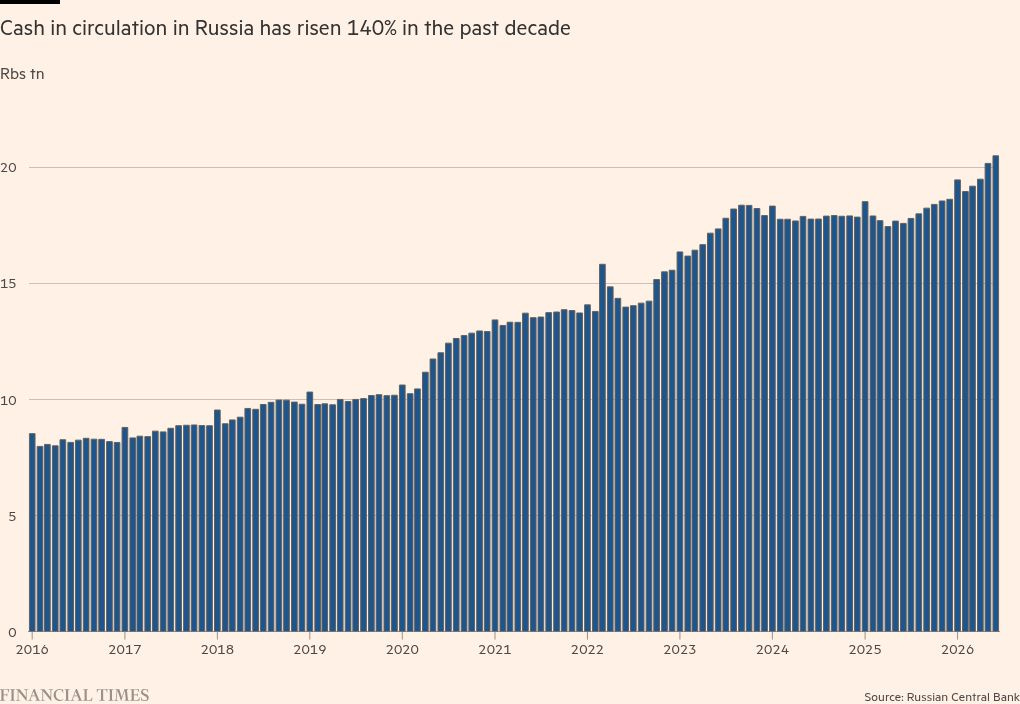

○ Internet blackouts are forcing Russians back to cash.

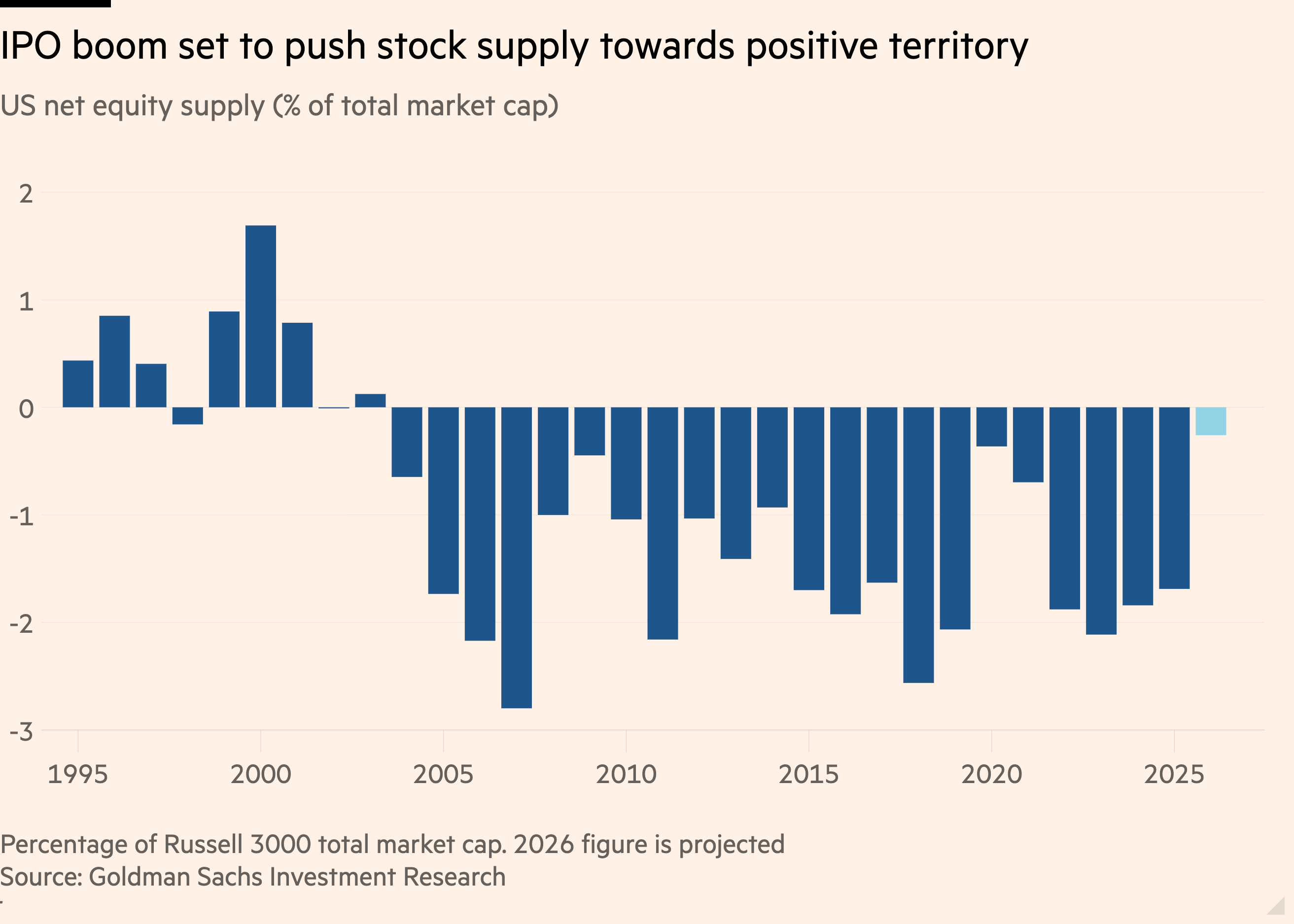

○ For the first time in a very long time, US stock markets might not shrink this year.

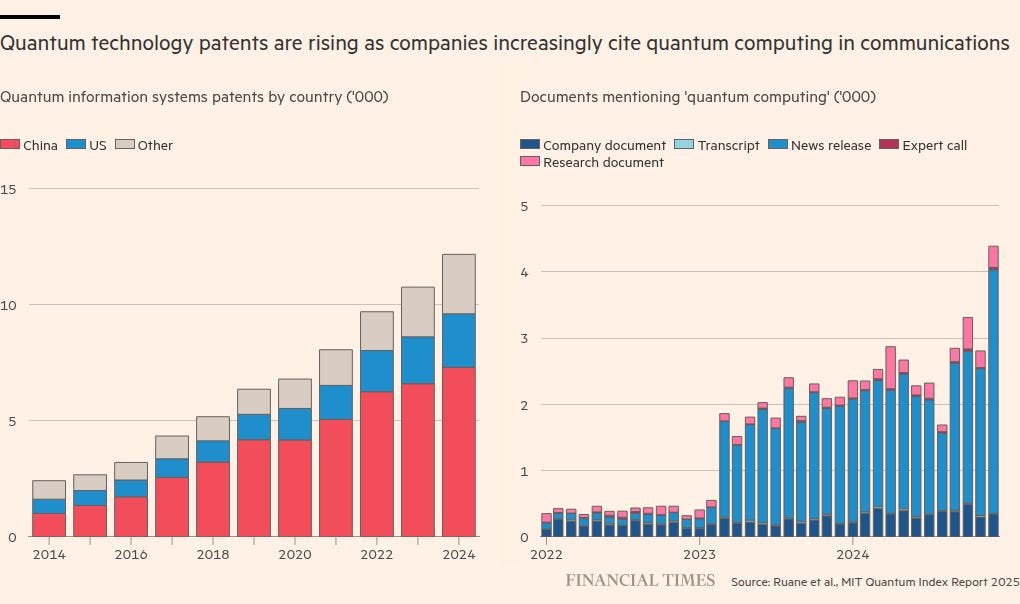

○ Commercial- and consumer-grade quantum computing may be a long way off, but a hype bubble is forming.

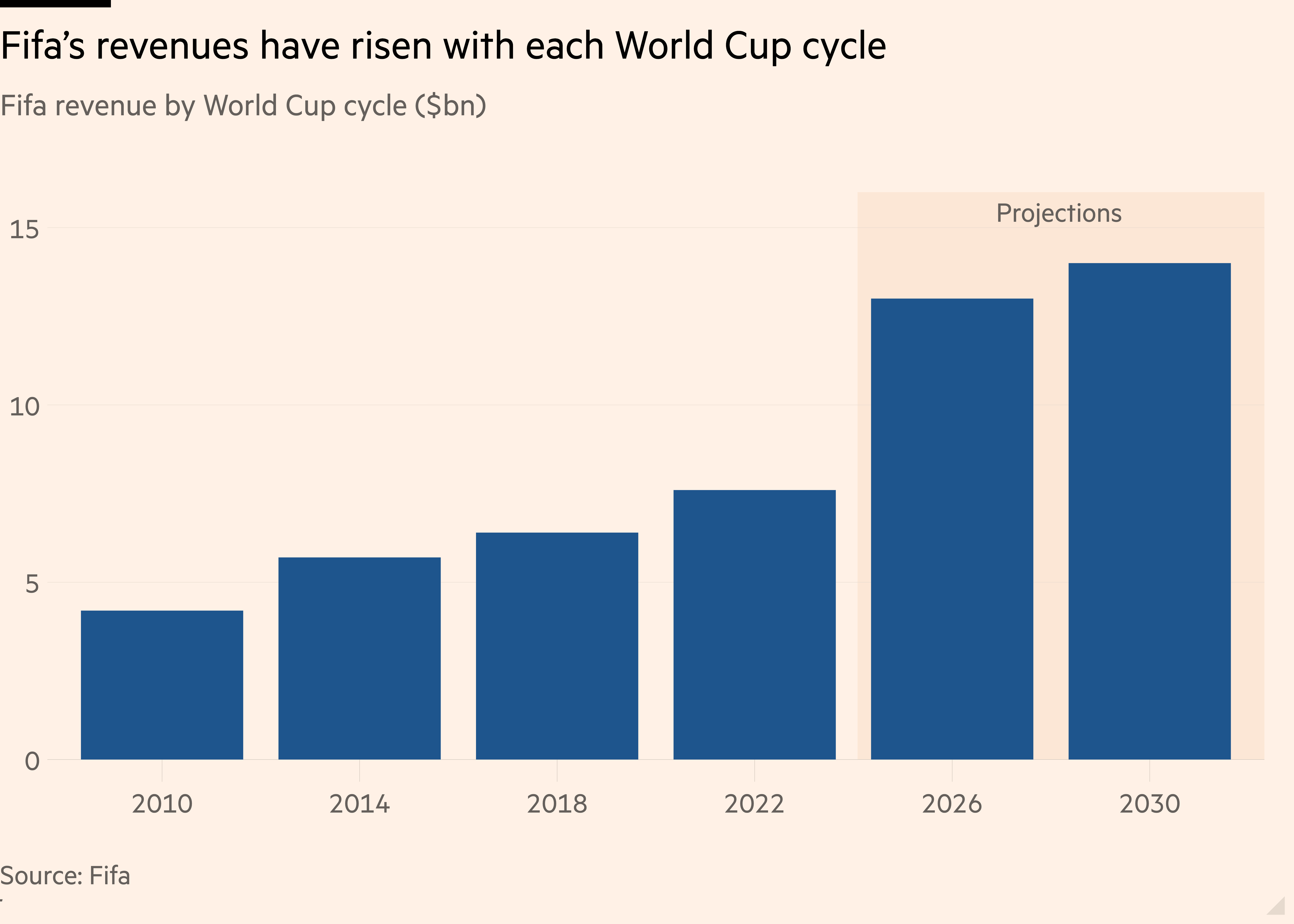

○ Ticket price gouging and association back scratching are allegations Fifa denies.

Great writing. Thank you for a morning gem.

10/10 for the Orb reference !!! 😃